Most teams don't struggle with what Scope 1, 2, and 3 emissions are. They struggle with navigating data complexity.

Which entities belong in your boundary?

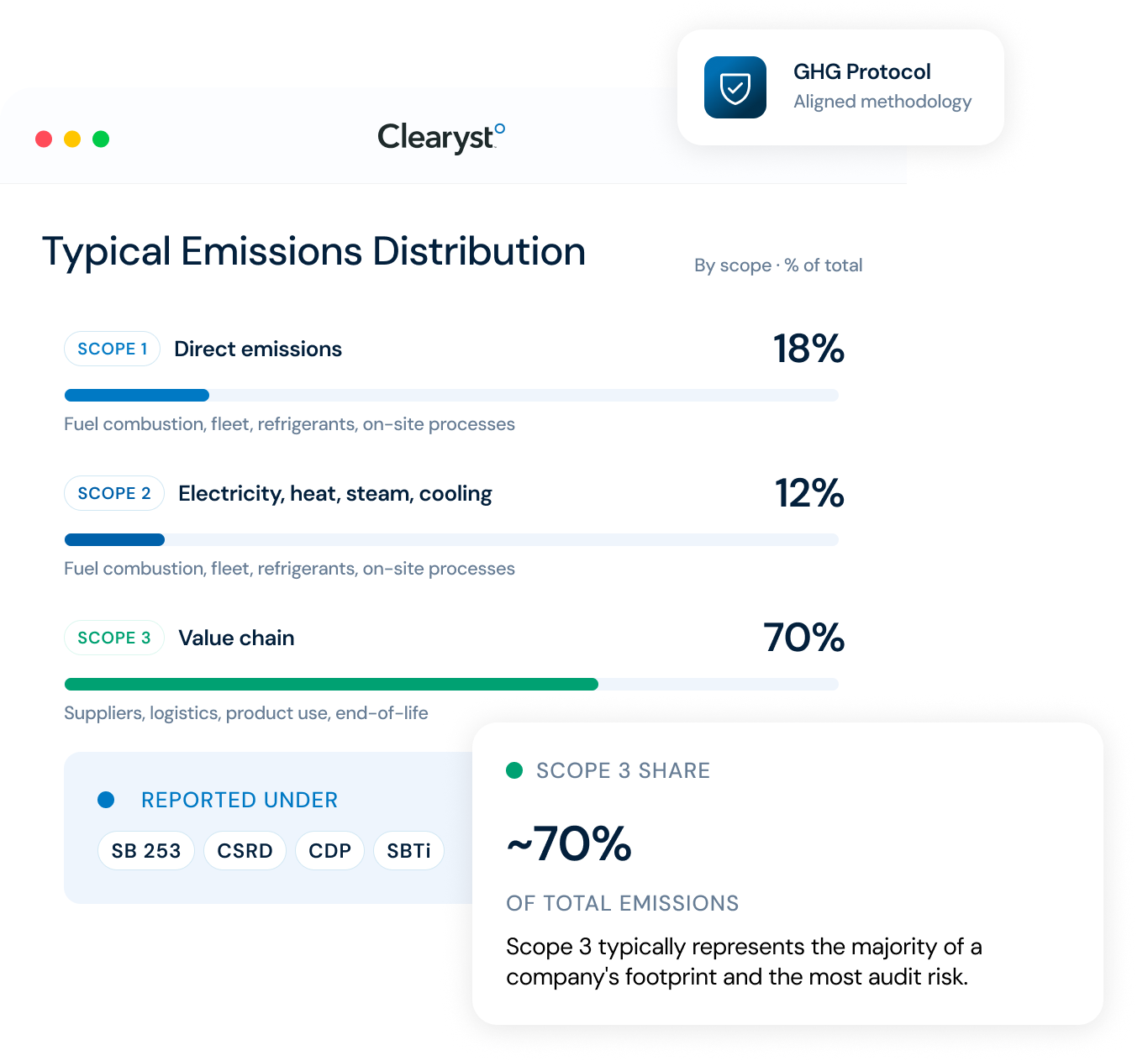

How do you ensure Scope 3 data accuracy?

How do you collect supplier data that holds up under scrutiny?

And once the numbers are calculated, will they pass assurance?

That's where Clearyst comes in. We help companies move from fragmented data and assumptions to structured, audit-ready emissions reporting.