02 GHG Inventory Development: Scope 1, 2, and 3

A systematic accounting of total greenhouse gas emissions across Scope 1, 2, and 3. The foundational requirement for compliance — and the most resource-intensive to build correctly.

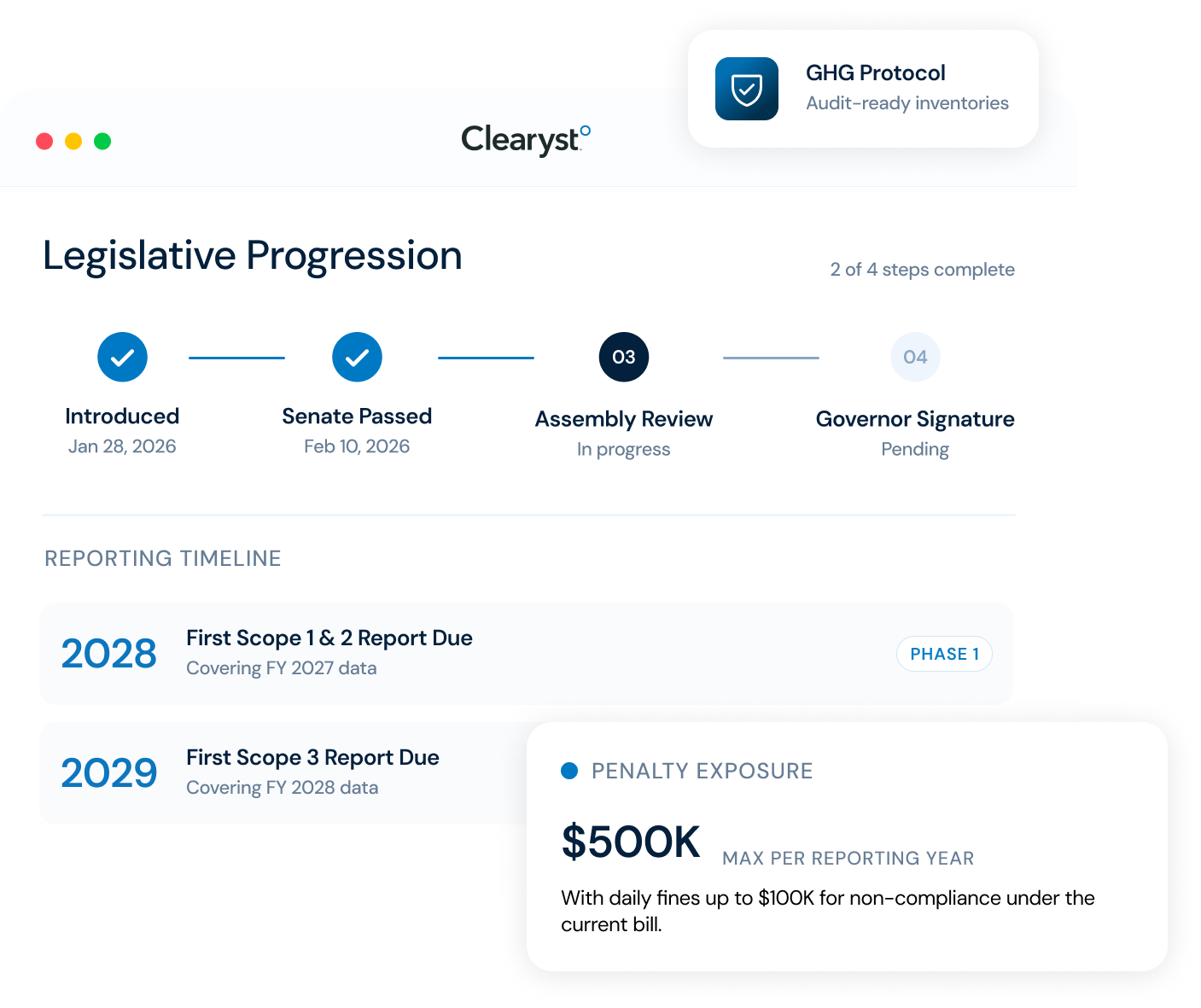

- Complete, audit-ready inventories aligned to GHG Protocol

- Scope 1, 2, and 3 emissions coverage

- Standardized methodologies across business units

- Repeatable, scalable data structures

Outcome: One inventory that supports NY, SB 253, and broader ESG reporting.